Emerging from COVID-19

What Will Shape the Geospatial Industry?

Which exciting opportunities lie ahead as the geospatial industry emerges from the COVID-19 pandemic? And what other influences are shaping the future of our sector?

The geospatial industry has been more fortunate than others – such as hospitality and tourism – during the COVID-19 pandemic. In fact, there are some exciting opportunities relating to accelerating the digital transformation so that businesses can adapt to the ‘new normal’ and economic stimulus packages with a greater emphasis on green growth. Furthermore, the health sector, which has long failed to exploit the potential of geospatial, has started to recognize its value. This article examines these and other influences that are likely to shape the future of the geospatial industry.

The COVID-19 pandemic has provided a warning about the very real risk of new crises of unforeseen nature emerging in the future. At a time when healthcare systems are under unprecedented pressure, geospatial solutions have proved essential in crisis management by supporting analysis of how the virus is being spread and by whom, as well as logistical challenges such as where personal protective equipment (PPE) is being manufactured and what supply chain is required to get it to where it is needed.

Personal privacy vs public health

As various public inquiries look at what their own nations could have done better, they will look East. Countries such as South Korea enacted legislation allowing government use of data from smartphones, social media and ride-sharing apps to help understand and control the spread of infection. Experience with SARS and, more recently, MERS led to democratic governments in the region overcoming privacy concerns and enacting laws to authorize emergency use of such data for public health purposes. In the West, we already trust our governments to collect and use – in strictly protected ways – vast amounts of our personal data during population censuses. The way they anonymize such data is well established and effective. So why, in the developed democracies of Europe, can we not trust our legislators to put in place such temporary measures for health emergencies?

Digital transformation

The most profound long-term change is likely to be the acceleration of the digital transformation, not only as underpinned by European Union declarations, but recognized globally. The rise of Zoom seems to have made companies more accepting of remote working almost overnight, resulting in a significant structural impact on the configuration of cities and public transport networks. The increasingly pervasive use of the term ‘artificial intelligence’ (AI) to underpin all use of advanced software engineering, whilst a troubling misappropriation of the term, does point to where geospatial can contribute to adapting to such change. An increasing interest in geoAI in the finance sector, for instance, will be part of a move to make better use of alternative sources of data for ‘decisioning’ on investment options. Another facet of digital transformation will be the increased use of drones. Surveyors may not be allowed to visit sites to undertake their work and crews cannot travel to a site together, but sending up a drone is OK. With less air traffic, aerial surveys around the busiest airports have also become easier.

Social and economic damage

As the world emerges from the pandemic, the huge social and economic costs will start to hit individual businesses and their employees. It has clearly been necessary for governments to substantially increase sovereign debt for job retention and other business support schemes, but that money will have to be paid back. Interest rates are currently low and the repayment periods for strong economies are relatively long. However, the danger is that inflationary pressures will grow as suppliers rack up prices to recover losses suffered during the pandemic.

Recent announcements of pay freezes for public-sector workers are a foretaste of cuts in public investment and tax rises. With public-sector organizations accounting for an estimated 50% of supply-side geospatial companies’ sales, this will affect revenues. For instance, there will probably be a slowdown in digital twin projects, which are often sponsored by city authorities, as discretionary spending is cut with the diversion of resources to social care. The situation is likely to be exacerbated by a reduction in new, large construction projects because of changes to living patterns. People’s desire for more outside living space will see the depopulation of cities over the next decade and the rise of smaller developments in satellite towns. The office-space needs will change for most geospatial companies due to the shift towards the ‘WeWork’ model to preserve community spirit and as face-to-face meetings are held less frequently and closer to home. This change will be accompanied by the conversion of large swathes of office space for residential or other uses.

Silver linings

Nevertheless, the clouds hanging over the infrastructure sector have a silver lining. The European Union Green Deal will drive massive investment in projects that have a positive environmental profile. This is not only good for the planet, but is also likely to stimulate the need for wide-ranging environmental impact assessments. The greening of agriculture will create the need for ever-more precise Earth observation data. Alongside this, the implementation of the global Financial Action Task Force (FATF) recommendations will mean financial institutions will have to report on climate-related risks as part of the stress tests imposed by regulators. In general, there is currently a relatively poor understanding of the location of the assets invested in by financial institutions. This will need to improve to meet these requirements. The Spatial Finance Initiative is a good source of further information on this potentially huge market for geospatial companies. It will require complex integration of Earth observation and human geography (statistics, mobility, address) and the application of machine learning to huge quantities of data. ConsultingWhere is currently authoring a joint report with the Satellite Application Catapult on this subject due for release in early 2021.

Market opinion

In the summer of 2020, ConsultingWhere conducted an opinion survey to test sentiment in the industry on prospects over the next few years. The respondents were mostly UK-based and represented about 100 separate organizations with a reasonably even spread, from small and medium-sized enterprises (SMEs) to large multinationals.

This was the third in a series of surveys and revealed some interesting results. COVID-19 is currently having a significant impact on the markets in which the respondents operate. Only 33% expected revenue growth in 2020, compared to 47% expecting their revenues to grow in 2021 and 70% in 2022. In the pre-COVID-19 survey in early 2020, 62% were expecting substantive growth over each of the following three years.

Sectoral contrasts

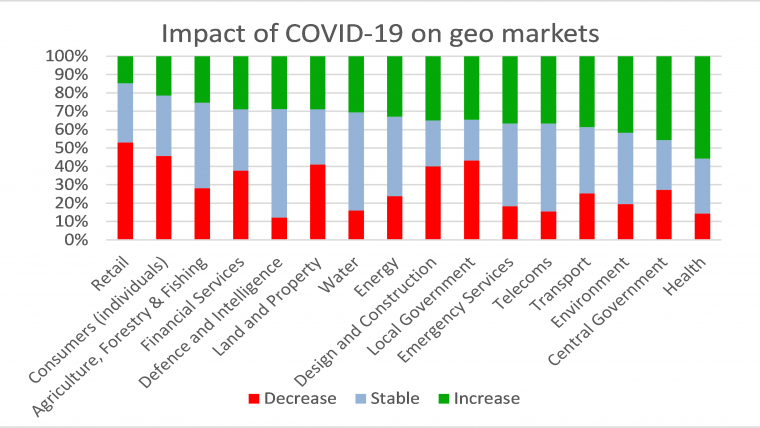

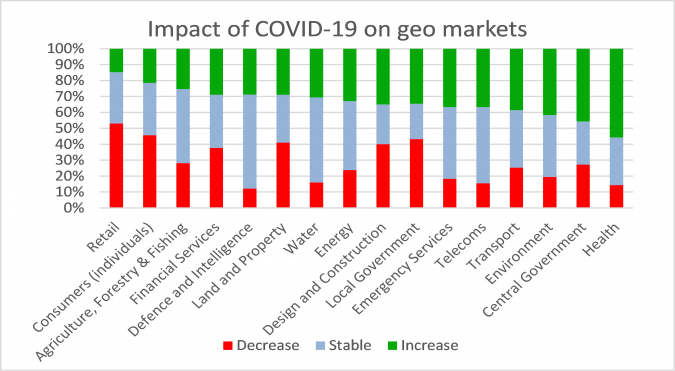

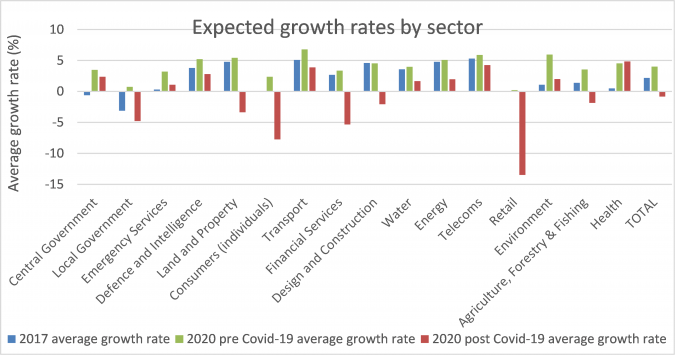

Based on the survey, there has also been a sharp change in the patterns of expected growth by sector. The survey indicates that more stable private sectors such as energy, telecoms and water are still expected to expand, as are central government, health and emergency services. On the other hand, sectors which are typically more sensitive to consumer behaviour are expected to contract – particularly retail but also construction, property and consumer mapping. Figure 1 summarizes the findings, organized from left to right in increasing confidence in future growth. Sectors with relatively high sensitivity to consumer behaviour predominate on the left of the chart, whilst those markets with lower reliance on consumer disposable incomes are shown on the right.

Timeline comparison

When the three recent surveys are viewed together, signs of the disruption to the upward trend in confidence become more clearly visible. Figure 2 compares the average expected growth rate by sector across the three surveys. In the 2017 survey, only two sectors were expected to contract – central government and local government – whereas a broad array of sectors are now expecting to suffer reduced demand over the next three years, some of which had high growth expectations in 2020.

Private sector

This data throws new light on the prospects for the more stable private sectors. Water, energy, transport and telecoms all show that growth levels have been cut from their pre-COVID-19 levels but by much less than their more cyclical counterparts. Each expects to remain positive in terms of overall market opportunity. Even within this seemingly homogenous grouping, there are subtle differences in the underlying responses. More respondents indicated that growth in transport was likely to be greater than 10%, better than in any of the other three sectors. This may reflect the potential for increased geospatial involvement in the growing market of delivery and collection businesses resulting from the move towards online shopping.

Public sector

Only the health sector has a higher average growth rate post-COVID-19 than before it. The central government sector has held onto some of the gains that had been accrued since 2017 but is down on the pre-COVID-19 expected growth rate. This is likely to reflect similar factors as healthcare in terms of increased focus on well-being outcomes. Pessimism on local government expenditure endures.

Conclusion

In summary, it is likely that the geospatial industry will prosper from the changes – both temporary and permanent – that are occurring as the world emerges from the pandemic. To use the current jargon, many businesses will need to ‘pivot’ their business models to focus on different sectors. This will involve moving out of their comfort zone to engage customers in new sectors and exploit the wide range of new technological advances coming out of the research community. If the industry does not adapt quickly, for sure others will move in to ‘eat our lunch’.

Further reading

https://ec.europa.eu/isa2/news/eu-member-states-sign-berlin-declaration-digital-society_en

Value staying current with geomatics?

Stay on the map with our expertly curated newsletters.

We provide educational insights, industry updates, and inspiring stories to help you learn, grow, and reach your full potential in your field. Don't miss out - subscribe today and ensure you're always informed, educated, and inspired.

Choose your newsletter(s)